How AI Is Changing The Consumer Buying Journey (And What The Data Shows)

I’ve been reading Similarweb’s new report, the 2026 AI Brand Visibility Index, and a number I keep coming back to, the one I think reframes the entire conversation about AI and marketing: 35% of US consumers now start their product discovery with an AI tool. Only 13.6% start with a search engine.

This means that for every three consumers who begin their buying journey, roughly one starts in ChatGPT, Gemini, Perplexity, or other AI chatbots. Fewer than half that number start in Google.

My instinctive response to data like this is to go on LinkedIn and post that SEO IS DEAD… again. I understand why people would look at this stat and frame it as an SEO threat, but I think that framing is too narrow.

AI did not replace the purchase journey, it restructured it.

The funnel still exists. Consumers still discover, research, evaluate, and buy. What changed is which tools dominate which stages, what that means for brand visibility, and, most interestingly to me, why the brands winning in AI responses are often not the ones you would expect based on their search presence.

In this article, I’ll work through what the data shows at each of the five funnel stages, which sectors have seen the sharpest disruption, what separates AI-visible brands from invisible ones, and a four-step framework grounded in what the Similarweb data actually shows works.

What the AI-assisted consumer buying journey actually means

The AI-assisted consumer buying journey is the process by which buyers use conversational AI tools to discover products, compare options, evaluate choices, and reach purchase decisions, often before engaging with a brand website or search engine. It does not replace human intent. It restructures the channels through which that intent is expressed and resolved.

That distinction is where I think a lot of the current strategic confusion originates. When marketing teams hear “AI is taking over the funnel”, they tend to either panic about SEO or dismiss it as hype, when the more useful question is: at which stages is AI taking share, from whom, and what does that mean for how you structure your content?

For two decades, brand visibility was defined by search ranking position. A brand with strong SEO appeared at the top of the results page when a consumer searched for a relevant term. The consumer saw the listing, clicked, and the brand had its shot.

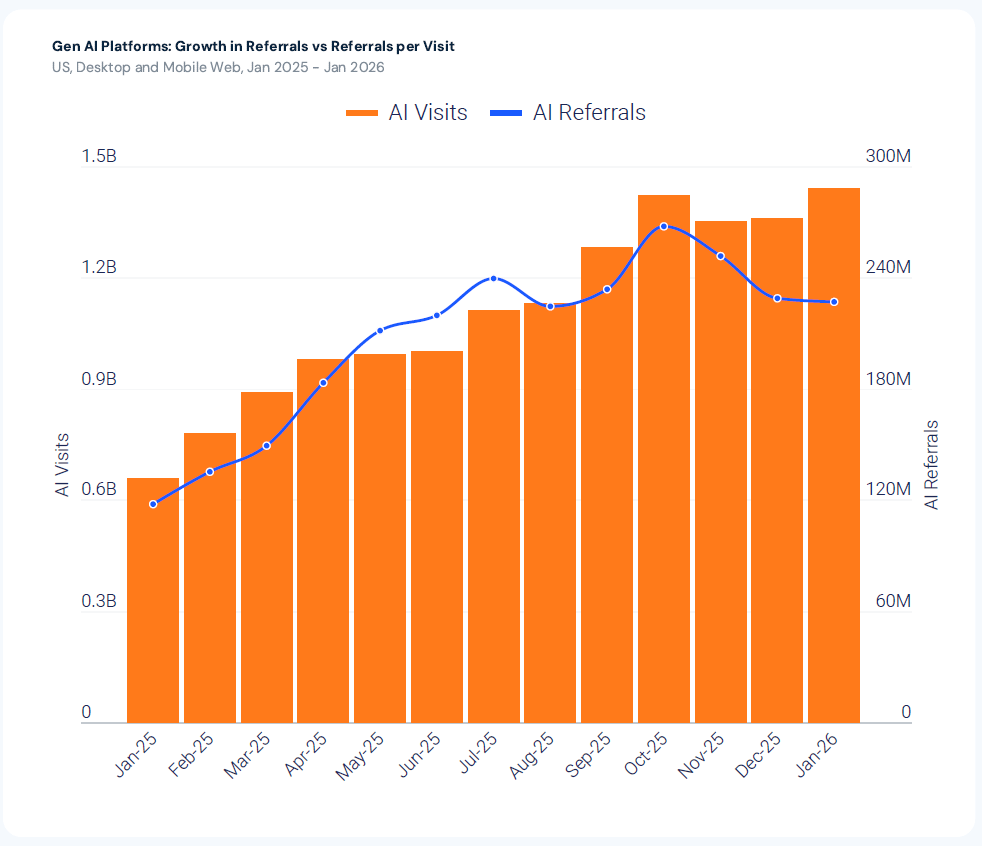

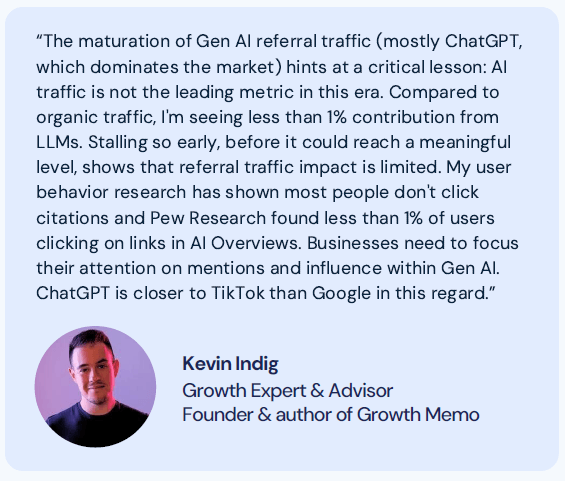

AI changes this in two ways. First, instead of presenting a list of options, AI presents a single synthesized answer. If a consumer asks “What’s the best noise-canceling headphone under $200?”, they get a recommendation, not ten blue links. Second, and this is what I find most revealing about where AI’s influence actually lives, AI referrals to external sites have plateaued even as visits to AI platforms keep rising. Between January 2025 and January 2026, visits to AI platforms grew by 28.6% in the US. Referral traffic from those platforms over the same period: flat.

Kevin Indig draws the implication clearly:

That reframe, from traffic to influence, from clicks to mentions, is the one I keep returning to. It changes what you measure, what you optimize for, and what constitutes success.

AI vs. search: what the data shows at each stage of the buying journey

What I find most valuable about our report is that it does not ask consumers what they intend to do. It measures what they actually do at each stage. When we surveyed US consumers on which tools they find most useful at each point in the buying process, the pattern that emerged was both cleaner and more nuanced than I expected.

A few things in this data are worth pausing on.

AI leads at every stage but the last. From initial discovery through value evaluation, AI holds a consistent 2:1 or greater advantage over search. The important nuance here is that this is not just a top-of-funnel story, which is how I often see it characterized. Consumers are using AI to narrow shortlists, evaluate confidence, and decide between specific brands, stages that traditional marketing models assigned to the brand’s own advertising, product pages, and review presence. That represents a big change in where brand influence needs to be established.

The funnel does not collapse into a single AI interaction. Each stage shows meaningful usage of both AI and search, which is worth holding onto when evaluating the “AI kills search” narrative. The more accurate picture, from my reading of this data, is that AI and search are used for different cognitive tasks at the same funnel stage. AI synthesizes and guides. Search navigates and verifies. They are less competitive and more sequential.

Search closes the final mile, but on AI’s shortlist. The gap narrows sharply at the purchase stage, where AI leads by only 2.2 percentage points. By the time a consumer is ready to buy, they return to search to navigate to specific sites, compare actual prices, and confirm availability. This is the part I think deserves more attention in strategy conversations: search is still doing conversion work, but it is executing on a shortlist that AI already assembled. Being absent at discovery does not mean losing the click. It means not being considered before the search bar opens.

Why last-click attribution hides AI’s role

This is the operational implication I find most teams are underprepared for, and it is worth being direct about.

Traditional attribution models assign conversion credit to the last touchpoint before purchase. On that model, AI is nearly invisible because AI rarely appears as the final click. A consumer discovers a brand in ChatGPT, reads about it in its answer, then executes a branded search before converting. The search click receives 100% of the credit. The AI mention that brought the consumer there is unrecorded.

This attribution gap means most brands are currently underestimating AI’s role in their pipeline. Our data shows that traffic referred from AI engines such as ChatGPT to transactional sites converts at higher rates than many traditional channels, a signal of elevated purchase intent in AI-referred visitors. Volume is low. Intent is high. And most analytics stacks are not yet set up to capture either.

Why some brands are invisible in AI responses (and what determines inclusion)

An important finding in our report is not which brands lead their sectors. It is the consistency with which smaller, specialist brands outperform household names when competing for AI citations rather than search rankings. That pattern holds across every sector we analyzed, Finance, Travel, Consumer Electronics, Beauty, Fashion, and News, and it is, to me, the finding with the most direct strategic implications.

Three patterns emerge from the data:

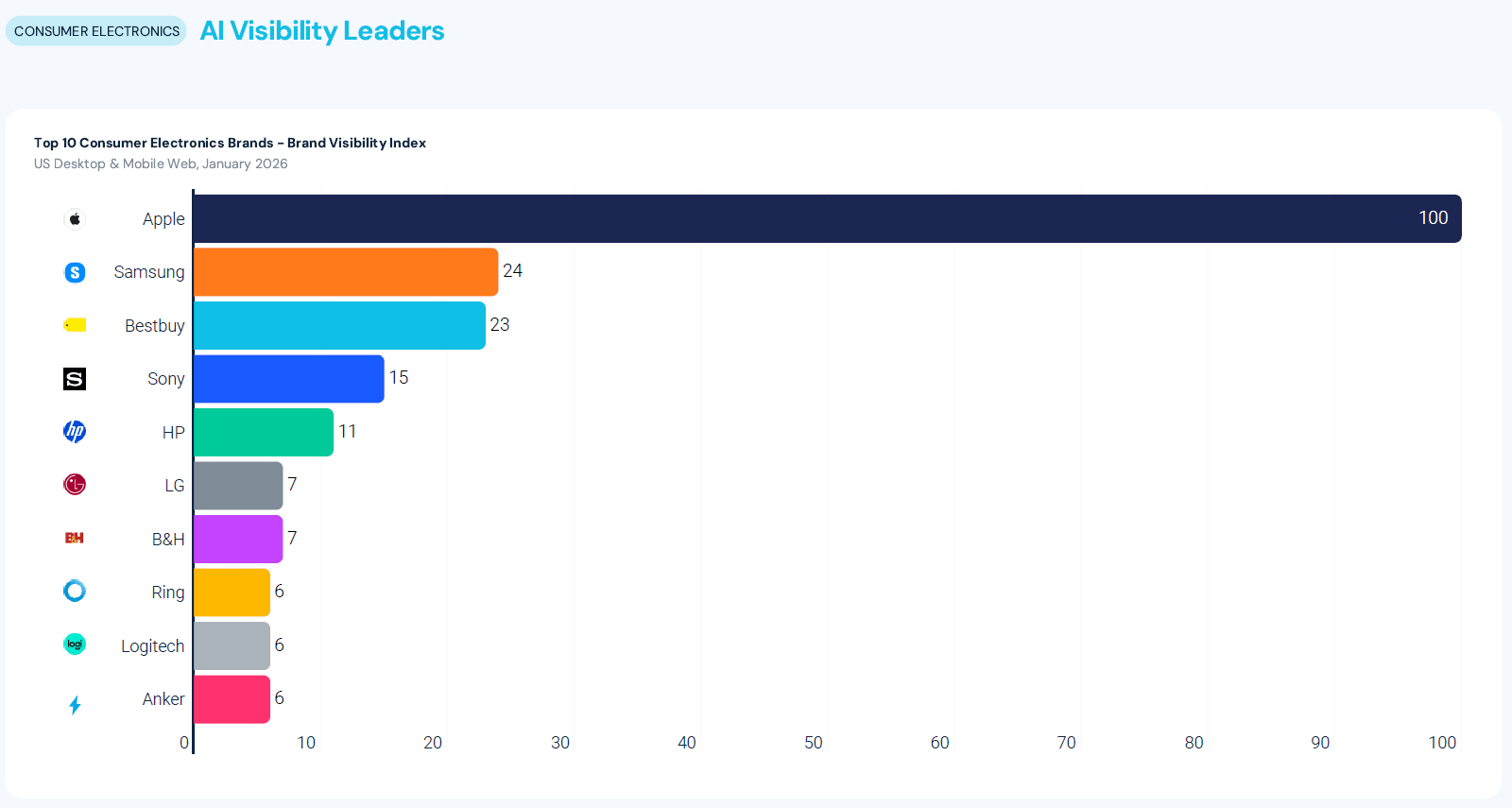

Visibility is highly concentrated. A small number of brands dominate AI mentions in each category, becoming default reference points in AI responses. In Consumer Electronics, Apple scores 100 on the Brand Visibility Index. Samsung scores 24. The 10th-place brand, Anker, scores 6. A 94-point gap between first and last. Once a brand becomes the default in AI, its advantage keeps growing.

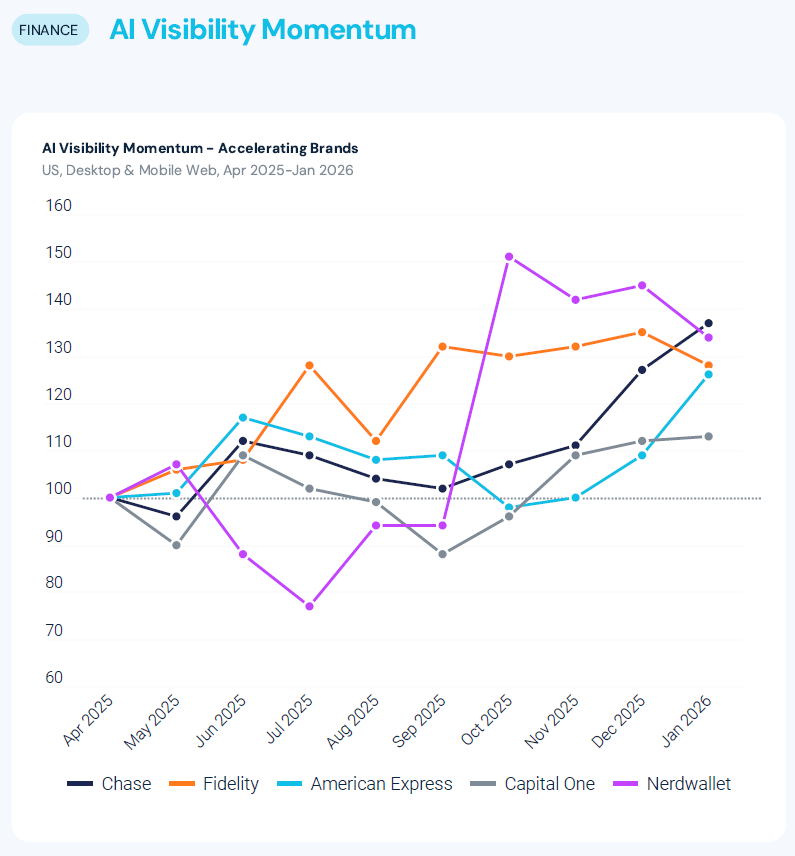

Momentum is uneven. Some brands are accelerating their AI visibility rapidly. Others are plateauing or declining, despite strong consumer awareness and search demand. In Finance, NerdWallet’s AI visibility momentum accelerated sharply between April 2025 and January 2026. PayPal, with far greater brand recognition, declined over the same period. The implication I draw from this is that AI visibility is an active discipline, not a passive outcome of having a well-known brand. Recognition built into search does not automatically transfer to AI.

Authority outperforms scale. In every sector, specialist or education-led brands rank significantly higher in AI visibility than their branded search demand would predict. In Finance, for example, comparison and reference-led platforms consistently appear above the parity line. Brand scale does not guarantee AI inclusion.

![]()

What I find interesting about this pattern is what it says about the nature of AI authority. The brands punching above their search-demand weight in AI visibility share a content model built around clarity, structure, and specificity. They will usually answer the question being asked completely, without assuming the reader has prior context. They organize information in a way that allows AI systems to extract and verify individual claims independently, something generic awareness content cannot do, regardless of how much of it exists.

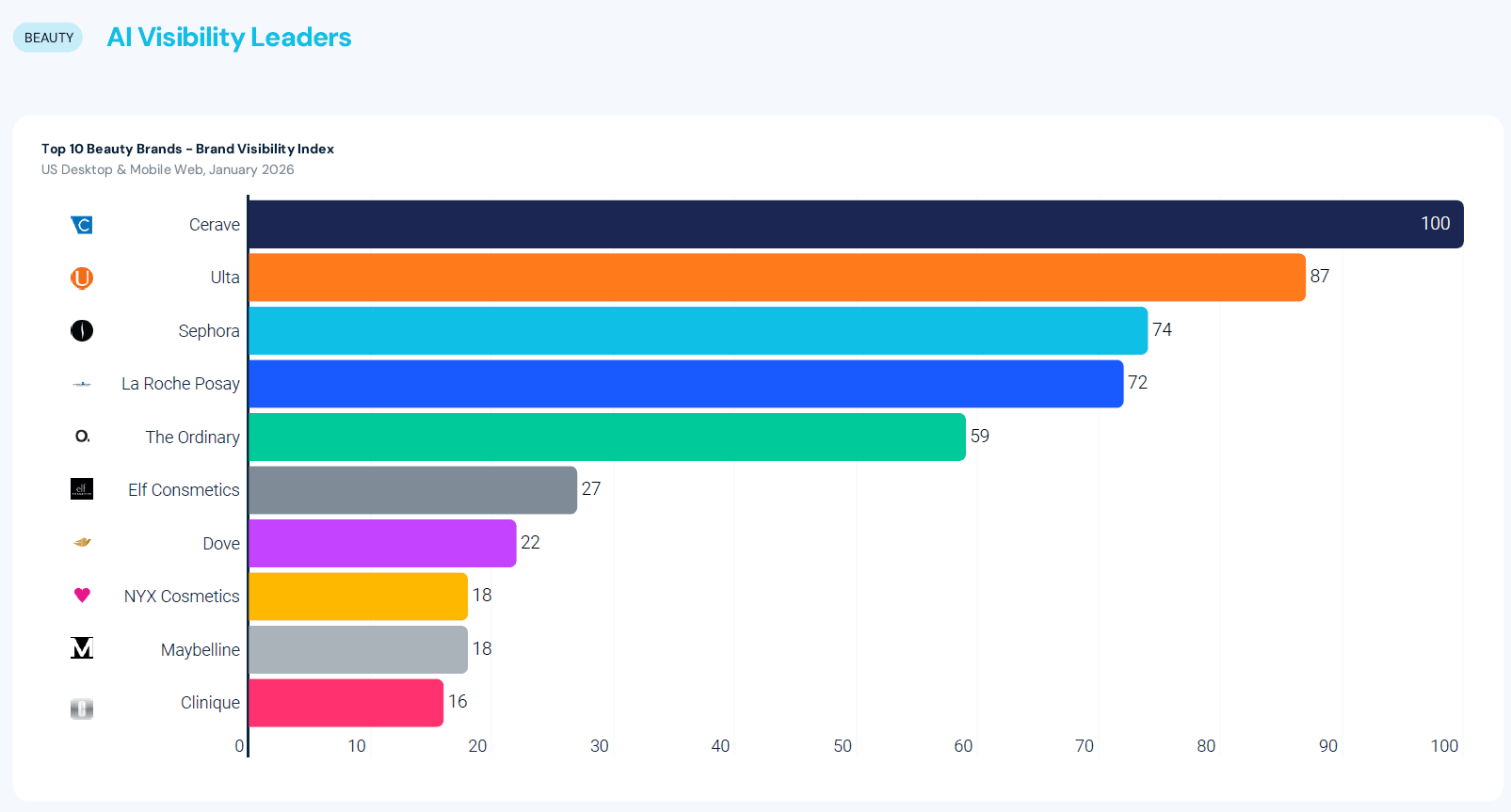

In the Beauty industry, CeraVe leads not because it outspends L’Oréal or Estée Lauder. It leads because its content addresses specific skin concerns with specific ingredient explanations in a format AI can parse, extract, and cite confidently. The same principle applies to Bankrate in Finance, Travelmath in Travel, and ScienceDirect in News. The common thread is not category, audience, or budget. It is content architecture.

Brands that block AI crawlers in robots.txt tend to underperform, even compared to brands with less content that’s easier to access. In other words, a smaller but open site can beat a larger one hidden behind paywalls or restrictions. Many teams haven’t fully considered this tradeoff yet.

The rise of agentic commerce: when AI stops recommending and starts buying

Agentic commerce refers to the practice where AI systems act on behalf of consumers, sourcing, comparing, and completing purchases autonomously, without the consumer visiting a brand website directly. It is no longer entirely a future scenario, and it is the development I find most strategically consequential for brands in high-consideration categories.

Gartner predicts that one in five purchases will be completed by an AI agent in 2026. In a survey of 1,300 US consumers conducted by Contentsquare in November 2025, 30% said they would be willing to let an AI agent complete a purchase on their behalf. In a separate study of US shoppers published in March 2026, 22% reported having already completed a purchase directly inside an AI tool.

The category specificity here matters for how you prioritize. Methodical, research-heavy purchases (appliances, financial products, software subscriptions, travel bookings) are more susceptible to agentic completion than impulse buys. These are precisely the categories where AI’s ability to process specifications, compare dozens of variables, and surface a constrained recommendation is most useful, and where the consumer previously spent the most time in the middle of the funnel.

For brands in these categories, the consequence is direct: a consumer whose AI assistant places an order on their behalf never visits the product detail page, never reads the brand story, and never sees an ad (Until ChatGPT rolls out ads, soon). The entire traditional brand relationship has been bypassed. As Bill Hunt, President of Back Azimuth Consulting, has noted, being “callable” through APIs and structured product feeds will be as critical in 2026 as being crawlable was in 2010, an idea now being formalized through emerging standards like the Universal Commerce Protocol (UCP), which aim to make seamless, agent-driven transactions possible across platforms.

Given how long it took most brands to take crawlability seriously after 2010, that comparison is instructive for how much runway there may actually be.

The brands building AI visibility today are building the advantage that will determine which products get selected by agents tomorrow. For practical guidance on making your products discoverable in AI shopping contexts, see our guide to optimizing ecommerce websites for ChatGPT.

A four-step framework for earning AI visibility in the buying journey

The data above describes what is happening. This section is about what to do with it.

Looking across the sectors in the Similarweb Brand Visibility Index, the brands overperforming in AI visibility share four main traits. They are not doing fundamentally different things than a good SEO content strategy requires, but they are applying those principles with greater specificity and, critically, measuring different outcomes.

Step 1: Audit your current AI presence

Before optimizing anything, you need to know where you stand. In practice, this step tends to get skipped because AI presence is harder to quantify than a search ranking. But it is the most consequential starting point, because without it, you are optimizing for assumed gaps rather than actual ones.

Tracking brand mention share means understanding the percentage of relevant AI responses in your category that include your brand name across ChatGPT, Gemini, AI Mode, and Perplexity, not just referral traffic from AI platforms.

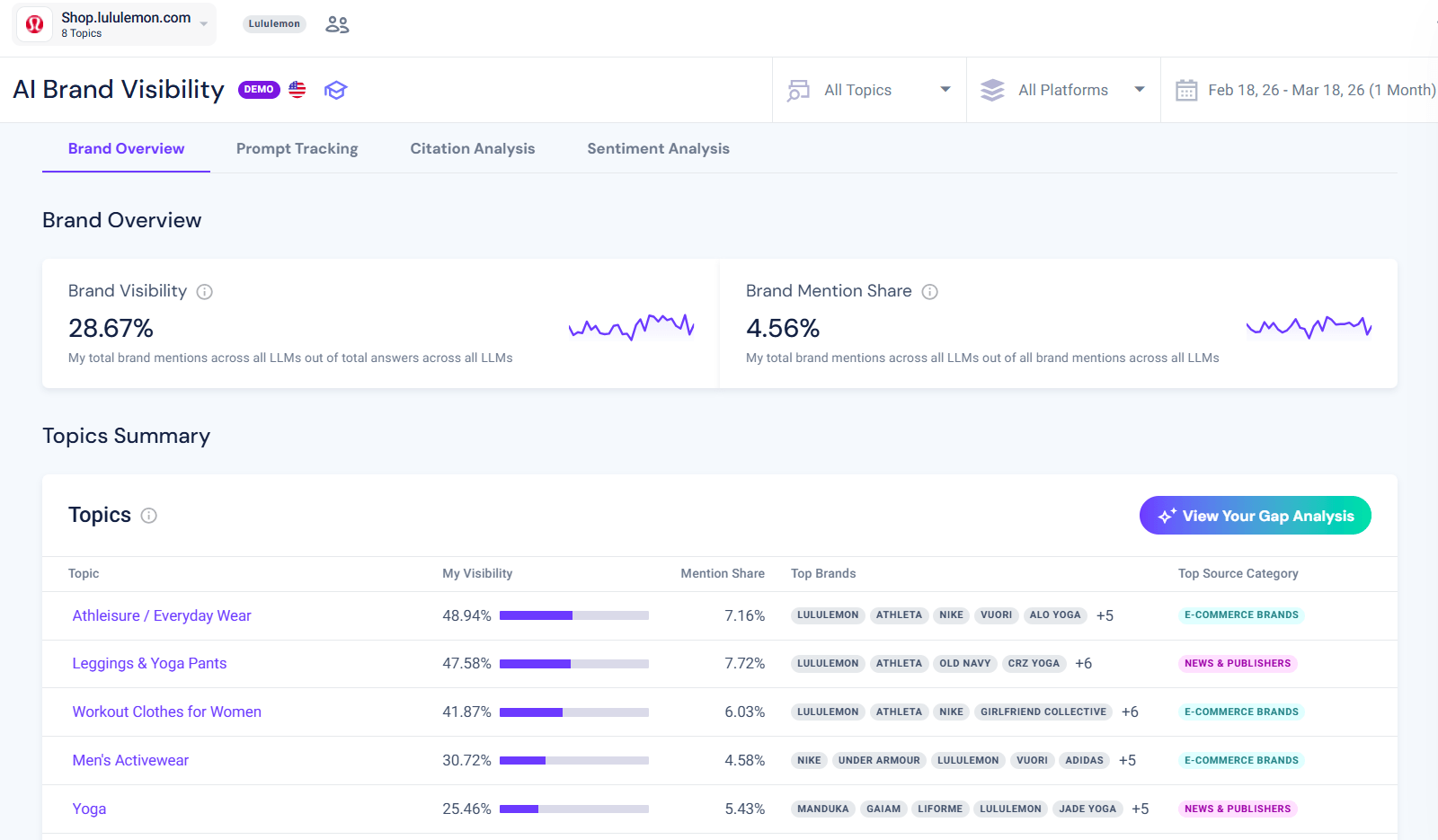

Similarweb’s AI Brand Visibility tracks this at the brand and category level, allowing teams to benchmark their AI mention share against competitors over time.

The goal of this audit is to answer three questions: Which queries trigger your brand to appear? Which competitor appears instead when your brand is absent? And which content on your site is currently being cited?

Step 2: Build topical authority clusters, not individual pages

This is where topical authority becomes important in AEO. AI systems do not evaluate brands based on a single page or keyword. They build confidence from repeated associations across a full topic cluster, including definitions, comparisons, use cases, and decision-stage queries. In practice, that means appearing consistently across the range of questions buyers ask, not just ranking for one term.

The structure of those questions follows a clear pattern:

As shown in this diagram, head queries are broad and competitive (“What is the best tool for X?”), while mid and long-tail queries become more specific and intent-rich (“best tool for X with Y” or with multiple constraints). Topical authority is built by covering this full spectrum, not just the high-volume head terms.

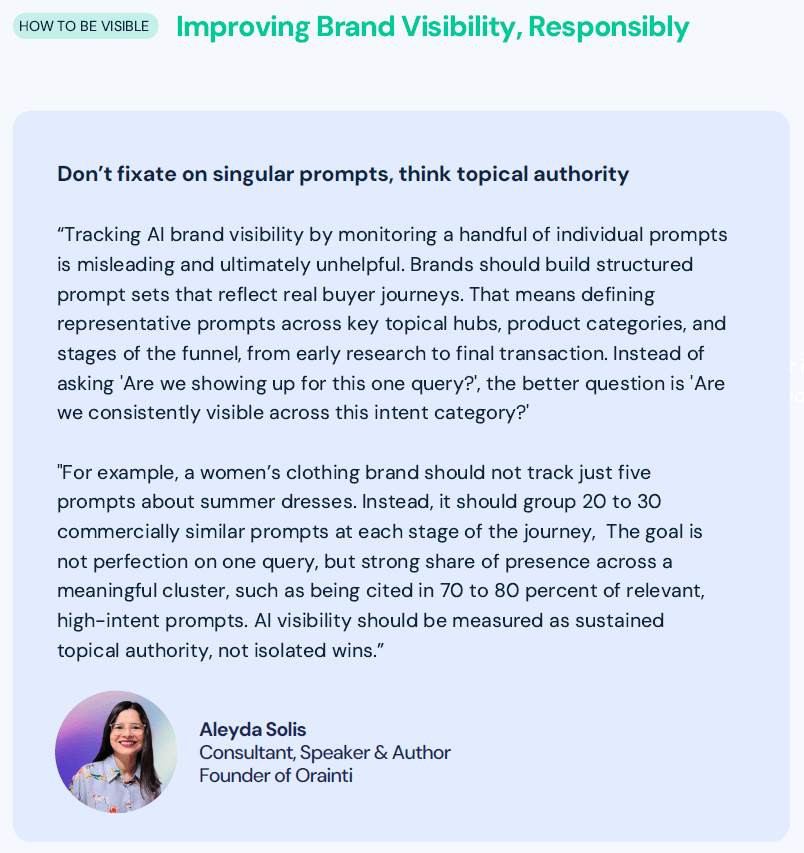

Aleyda Solis frames the measurement challenge in a way I find useful for teams trying to operationalize this:

In practice, this means mapping the buying journey for your category: the discovery questions, the comparison questions, the objection questions, and the “where to buy” questions. Each stage generates its own question types, and each type needs content that can be extracted without requiring the reader to have read everything before it.

Step 3: Win off-site consensus, not just owned rankings

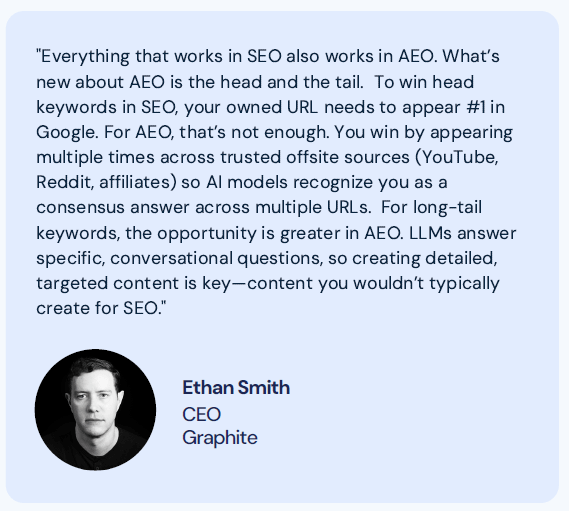

Ethan Smith, CEO of Graphite, identifies the big difference between SEO and AEO at the head-term level, and it is a distinction that I think GEO and SEO teams need to work through together:

AI systems see frequent, consistent mentions across independent sources as a sign of authority. Brands that show up positively on review sites, publisher content, forums, and data platforms gain visibility faster than those relying mostly on their own content.

This is similar to how Google values backlinks, but AI can factor in recent user sentiment much faster. That means PR and content need to work together around the same authority signals, not separately.

Step 4: Track mention share, not referral traffic

The final step is changing how you measure success, and this is where most teams struggle. Not because they disagree, but because new metrics change what gets reported, which affects stakeholders.

Kevin Indig’s observation that AI platforms deliver less than 1% of organic traffic levels in referrals means that brands using last-click analytics to measure AI performance are measuring the wrong thing. AI is influencing the buying journey at stages that never generate a trackable click.

Read more: GEO KPIs: What Are The GEO Metrics SEOs Should Know And Measure?

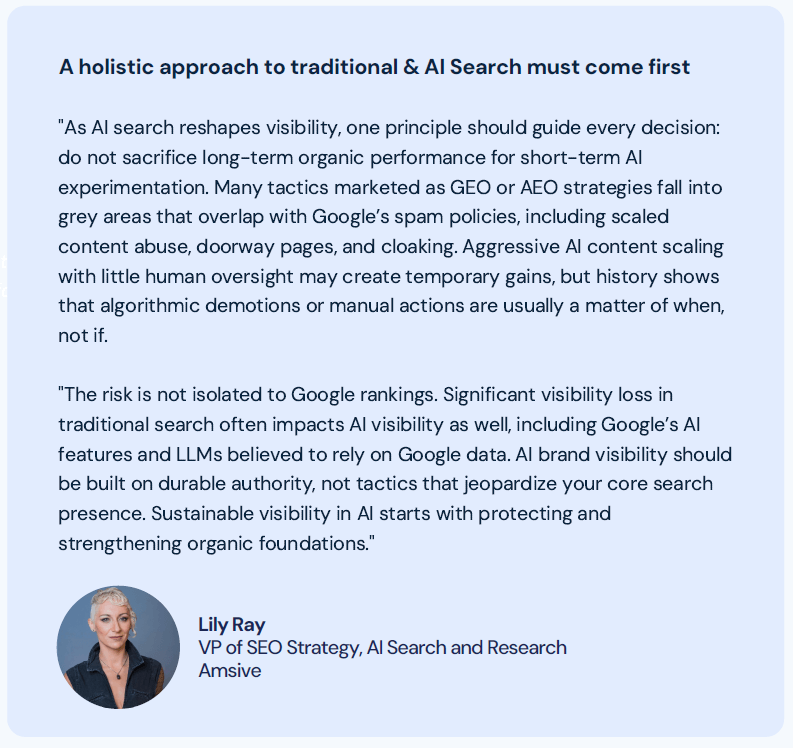

The metric that captures AI’s actual influence is brand mention share: how often does AI name your brand when discussing your category? Lily Ray, VP of SEO Strategy and Research at Amsive, provides a guardrail worth heeding:

These two channels aren’t competingת they reinforce each other. Content that ranks well in search is often the same content that earns AI citations, since both reward expertise, clarity, and clear authority signals.

The difference is in execution: AI favors standalone sections (sometimes referred to as content chunks), clear definitions, data-backed claims with sources and dates, and open access for crawlers. These are just refinements of strong content fundamentals, the core approach stays the same.

What this means for your strategy in 2026

The consumer buying journey has not disappeared. The same fundamental steps, discover, research, narrow, evaluate, buy, remain intact. What has changed is where those steps begin, and who shapes the shortlist before search ever enters the picture.

Adelle Kehoe, Director of Product Marketing at Similarweb, sums up this change clearly:

“AI Brand Visibility must now be embedded into every marketing team’s measurement framework, tracked consistently, benchmarked competitively, actively optimized, and reported at the leadership level. Visibility as a performance metric is not transient; it is a fundamental indicator of brand influence online”.

The brands accelerating in AI visibility across Finance, Travel, Electronics, Beauty, Fashion, and News are not the largest brands in their categories. They are the most legible ones, to systems that now decide which brands consumers consider before the search bar is ever opened. That is, to me, the most important strategic implication in all of this data: AI visibility is not an adjunct to brand strategy. It is increasingly where brand strategy begins.

The question, at this point, is not whether your audience uses AI in their buying journey. The data is clear that they do. The more useful question is whether AI has enough structured, citable, corroborated information about your brand to include you in the answer when they ask.

Track where your brand appears in AI responses for your category with Similarweb’s AI Search Intelligence, and explore the full 2026 data across six sectors in the Similarweb Generative AI Brand Visibility Index.

FAQs

At which stage of the buying journey does AI have the most influence?

AI’s greatest advantage is at the initial discovery stage, where 35% of US consumers use AI tools compared to 13.6% for search engines, according to Similarweb’s Market Research Panel (US, January 2026). This 2.6x advantage at discovery means AI is shaping shortlists before search receives any intent signal. The advantage holds through the evaluation stage (32.9% AI vs. 15% search) before narrowing at final purchase (24.3% AI vs. 22.1% search).

Does AI replace search in the buying journey?

No. AI and search serve complementary roles that reflect different task types. AI dominates the upper funnel, discovery, research, comparison, and evaluation. Search closes the final stage, finding where to buy and the best price, where AI leads by only 2.2 percentage points. The consumer buying journey starts in a conversation and ends in a search bar. Both channels need to be won.

What happens when a consumer sees a brand mentioned in an AI response?

After an AI tool mentions a brand, 40% of consumers search Google for more information about it, 36% use Google to compare it with alternatives, 34% ask the AI follow-up questions, and 28% go directly to the brand’s website. Only 8% ignore the mention entirely. Being named in an AI response initiates a multi-channel verification sequence, not a single click.

What is brand mention share, and why does it matter?

Brand mention share is the percentage of relevant AI responses in a defined category that include a brand’s name across ChatGPT, Gemini, and other AI chatbots. Similarweb’s AI Brand Visibility measures this at the brand and sector level. It matters because AI referral traffic represents less than 1% of organic traffic levels, meaning the impact of AI on brand consideration is primarily invisible to last-click analytics. Brand mention share is the metric that captures AI’s actual influence on the buying journey.

Which types of brands tend to win in AI visibility?

Across six sectors analyzed in Similarweb’s 2026 AI Brand Visibility Index, the brands with disproportionately high AI visibility relative to their search demand share three traits: they publish structured, deep content that AI crawlers can extract; they maintain strong third-party citation presence across publishers, review platforms, and user-generated content sites; and they provide open access to AI crawlers rather than blocking them. Specialist and education-led brands consistently outperform larger incumbents.

Related Posts

What Is AI Share of Voice? The Brand Mention Share Metric You’re Probably Missing

Wondering what Similarweb can do for your business?

Give it a try or talk to our insights team — don’t worry, it’s free!