Generative AI Statistics for 2026: The Latest Trends & Data Insights

2026 is the year AI stopped being a search story and became a brand visibility story. The platforms are no longer just growing, they are reshaping where consumers discover products, form opinions, and make decisions. The question is no longer whether your audience uses AI. It is whether AI knows who you are.

Similarweb has just published the 2026 Generative AI Brand Visibility Report, the first report to measure AI brand visibility at the sector level across Finance, Travel, Beauty, Electronics, Fashion, and News. It tracks which brands are being named in AI responses, which are being ignored, and what separates the two.

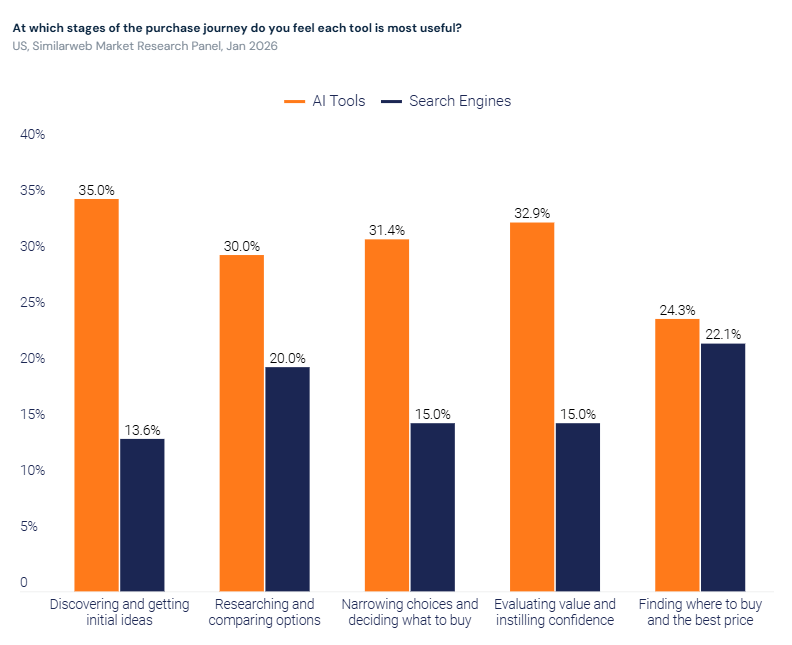

The numbers tell part of the story. AI tools now dominate the consumer purchase journey at every stage except the final transaction, 35% of US consumers use AI at the product discovery stage, compared to just 13.6% who use search. At the evaluation stage, that gap holds: 32.9% AI versus 15% search. By the time a consumer reaches a search engine, the shortlist is already set.

But the more revealing shift is happening beneath the surface, in which brands get named, which get ignored, and why the answer has very little to do with who dominates traditional search. Brand scale is no longer a reliable predictor of AI visibility. A dermatology-focused skincare brand outranks mass-market giants in Beauty. A wire service with a fraction of a major newspaper’s readership leads the entire News sector. A financial comparison site holds an AI rank 66 positions higher than its search rank.

Let’s start digging in.

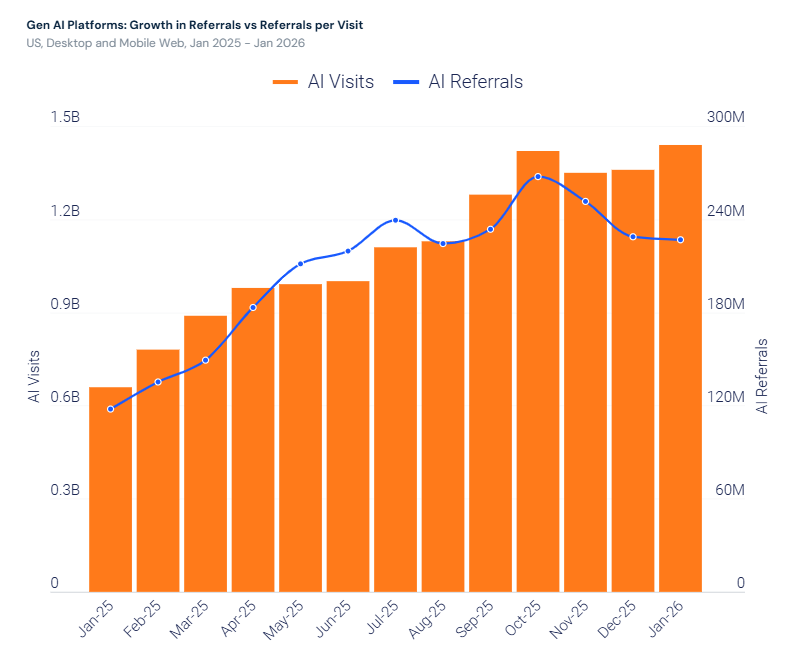

AI referral traffic has plateaued, and that reframes the entire metric

AI platform visits grew +28.6% between January 2025 and January 2026 (US, desktop and mobile combined), according to Similarweb data. AI referrals to external sites over the same period: flat.

Those two facts, side by side, tell a specific story. More people are using AI platforms more often, but they are not clicking through to other websites at a higher rate. The platforms are retaining attention, not distributing it. This is not a temporary lag, it is the intended design. AI platforms are built to answer, not to route.

“AI traffic is not the leading metric in this era. Compared to organic traffic, I’m seeing less than 1% contribution from LLMs. Stalling so early, before it could reach a meaningful level, shows that referral traffic impact is limited. My user behavior research has shown most people don’t click citations and Pew Research found less than 1% of users clicking on links in AI Overviews. Businesses need to focus their attention on mentions and influence within Gen AI. ChatGPT is closer to TikTok than Google in this regard.”, Kevin Indig

The referral plateau is not a failure of AI platforms. It is a structural feature. Generative AI is designed to synthesize and answer, not to route. When a user asks ChatGPT whether CeraVe or La Roche-Posay is better for sensitive skin, they get an answer. They may not need to click anything. The brand that appears in that answer has won something real, influence over a purchase decision, without ever receiving a referral visit. The brand that does not appear has lost that decision before the consumer ever reached their website.

The Visibility-over-Traffic (VoT) shift

The practical implication is a KPI change. If your team is measuring AI performance by referral traffic volume, you are measuring the wrong output. The new leading metric is brand mention share, what percentage of relevant AI responses include your brand. Similarweb’s AI Search Intelligence tracks this at the brand and category level, allowing teams to benchmark their AI visibility against competitors over time.

One caveat worth holding: when AI does send traffic, it sends high-intent traffic. Users referred from ChatGPT spend an average of 15 minutes on site versus 8 for Google referrals, generate 12 pageviews per visit versus 9, and convert to transactional sites at a 7% rate versus 5% from Google. Volume is low, but quality is measurably higher.

AI now owns the top of the consumer purchase funnel, search closes the sale

Similarweb’s Market Research Panel (US, January 2026) measured how consumers use AI tools versus search engines at each stage of the purchase journey. The results settle a debate that has been running since 2023: AI is not replacing search. It is replacing the top of the funnel that search never served particularly well.

AI holds a 2:1 or greater advantage at every stage from discovery through evaluation. At the final step, finding where to buy, the gap closes to near parity (24.3% AI vs. 22.1% search). The consumer journey is no longer starting in a search bar. It is starting in a conversation.

This has a direct consequence for content strategy. If 35% of initial brand discovery now happens through AI responses, then a brand that does not appear in those responses is invisible to more than a third of potential customers before any intent signal reaches search. AI visibility is not a supplement to SEO. For upper-funnel brand building, it has become the primary channel.

What this also means for attribution: the last-click model understates AI’s role in conversion. A consumer may discover a brand through an AI response, research it through AI, and only then visit the website via a branded search. The search click gets the credit. The AI mention made the sale possible.

Brand visibility stats by sector: the 2026 AI index

Similarweb’s 2026 AI Brand Visibility Index measured brand mention share across ChatGPT, Gemini, Copilot, and Perplexity, across six sectors in the US, using January 2026 data. Three patterns appear across every sector without exception: visibility is concentrated at the top, momentum is uneven, and content authority can outperform brand scale.

The gap column is the most important number in this table. A 94-point spread between first and tenth in Electronics tells you the sector is effectively owned by one brand. A 56-point spread in Travel tells you the top 10 is genuinely competitive. Before building an AI visibility strategy for any sector, the concentration gap tells you how much room actually exists.

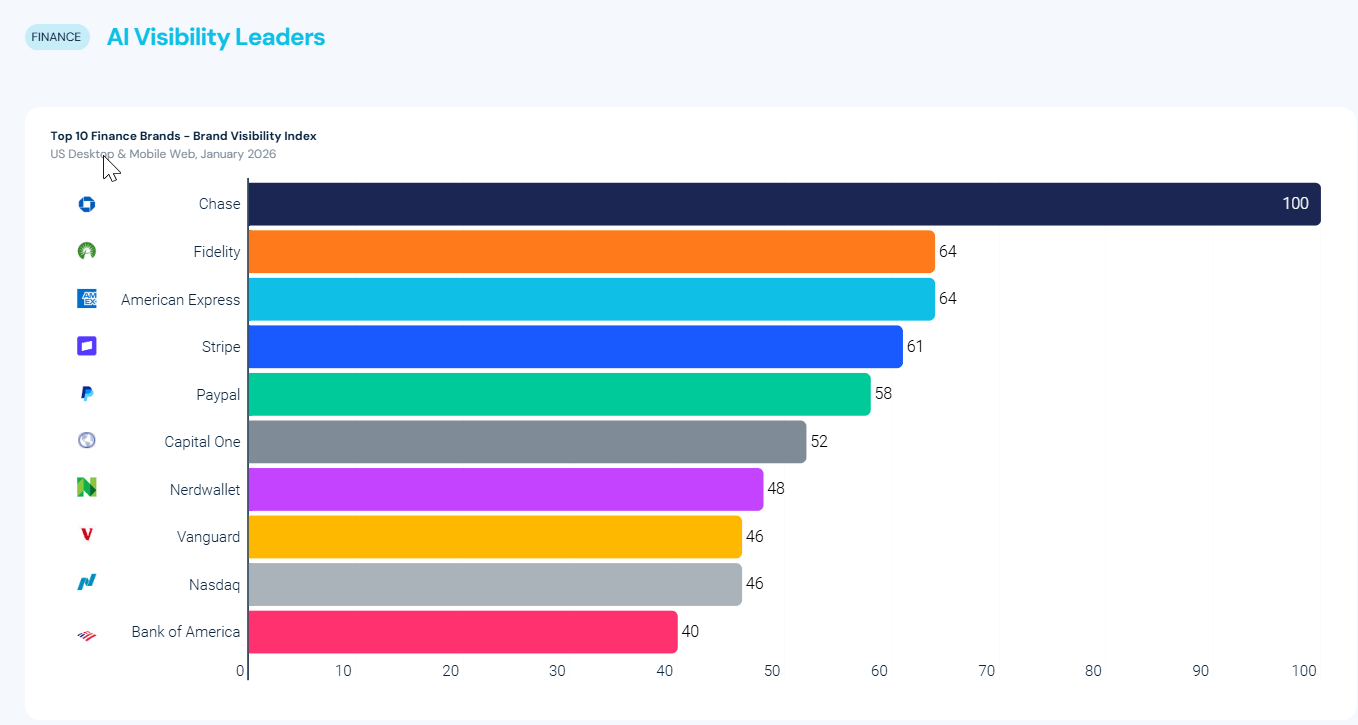

Finance: authority and scale coexist at the top

Chase leads with a 15.89% mention share across 11,073 prompts analyzed. What makes Finance distinctive is that structured-content platforms, NerdWallet, Bankrate, and Nasdaq, appear in the top 10 alongside institutional giants. In a sector defined by rates, comparisons, and regulatory complexity, explanatory depth carries real weight.

Finance is the sector that most clearly demonstrates the Authority Over Demand principle in action: the brands that explain things well compete directly with the brands that simply have the most customers.

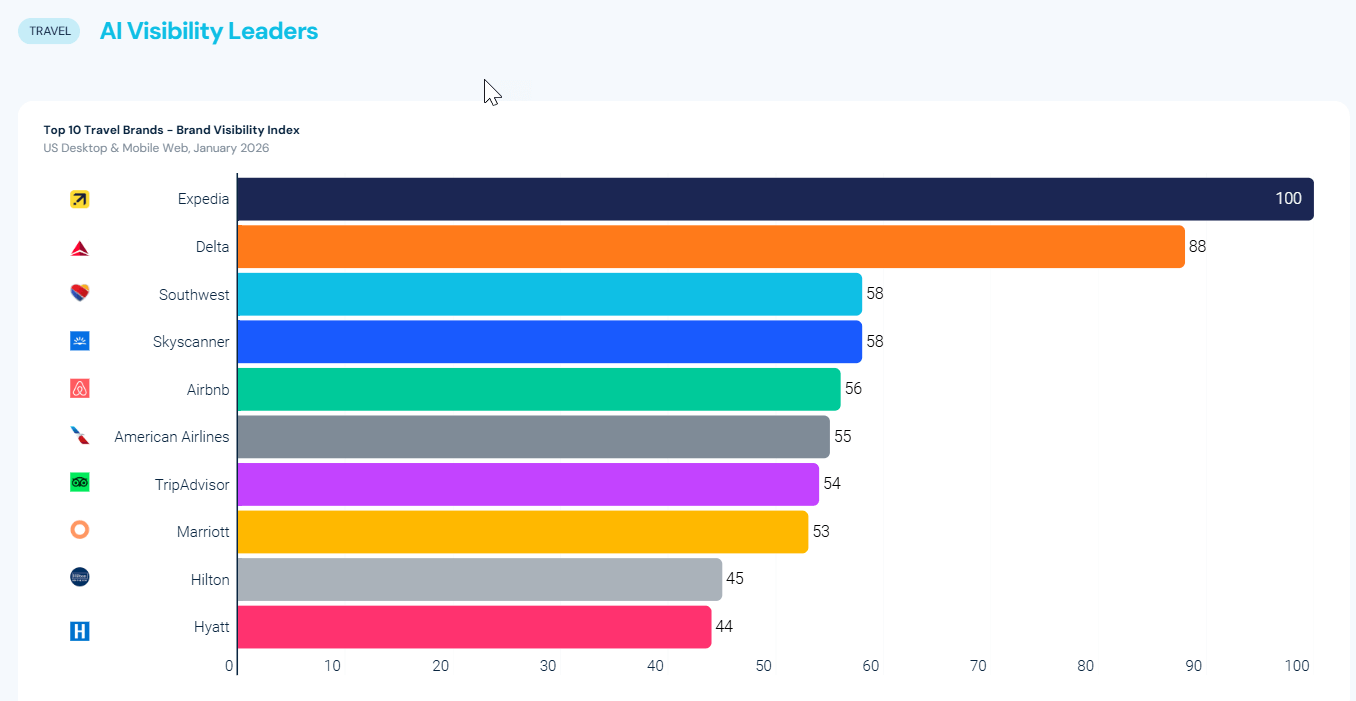

Travel: planning utility outperforms hotel brand scale

Expedia leads with an 18.18% mention share. Skyscanner and TripAdvisor both rank in the top 10 despite relatively low branded search volume, because they serve the planning and comparison use cases that AI handles best. Airbnb and TripAdvisor are both declining in AI momentum, a warning signal for platforms that grew on SEO-driven discovery.

The broader lesson for Travel: brands built around inspiration and community are losing ground to brands built around utility and structured trip logic. AI does not browse, it calculates.

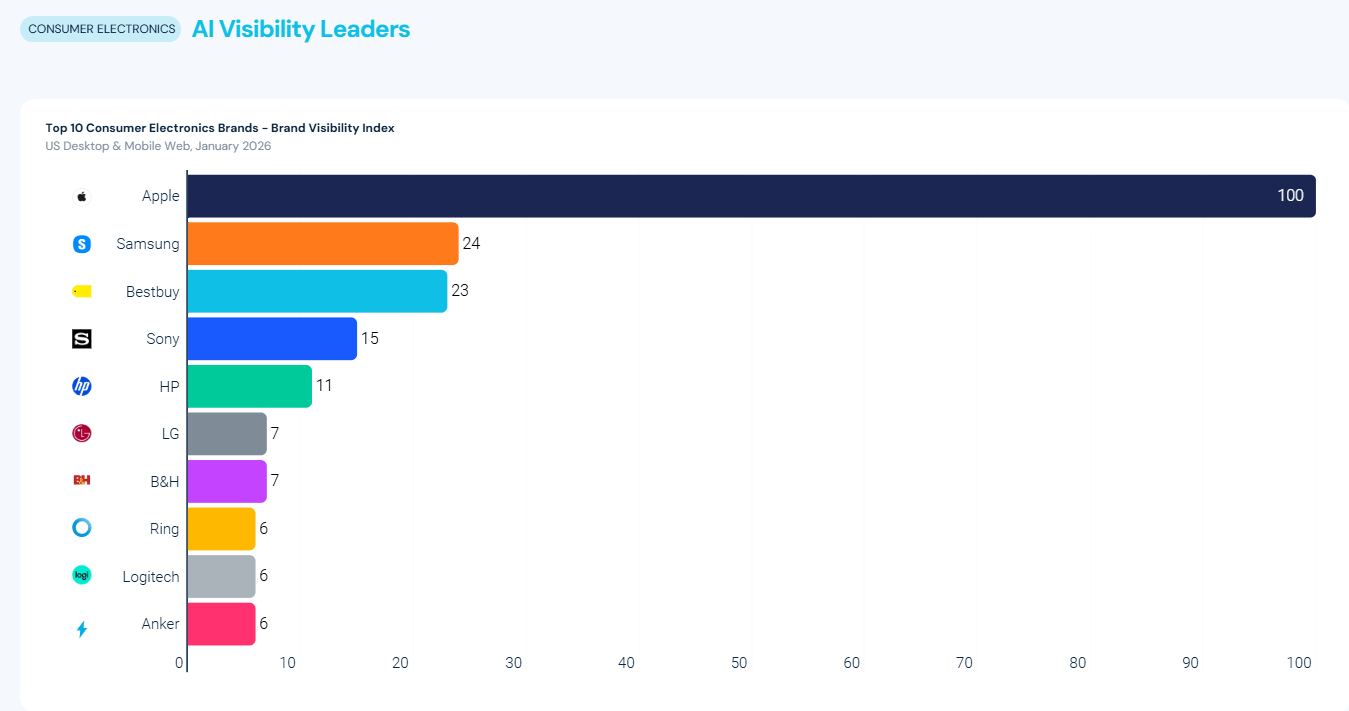

Electronics: Apple is cited in more than half of all responses

Apple’s 54.38% AI mention share is not a market leadership stat, it is a structural dominance stat. Samsung’s index score represents the second-largest drop from a sector leader in the entire index. The gap between Apple and tenth-place Anker is the most extreme concentration of any sector analyzed. For non-Apple brands, the only viable path to AI visibility is specialist content authority, troubleshooting guides, technical comparisons, setup walkthroughs.

Trying to compete with Apple on brand mentions is the wrong game. The opportunity is in owning the questions Apple does not answer, setup problems, accessory comparisons, repair guides, ecosystem alternatives.

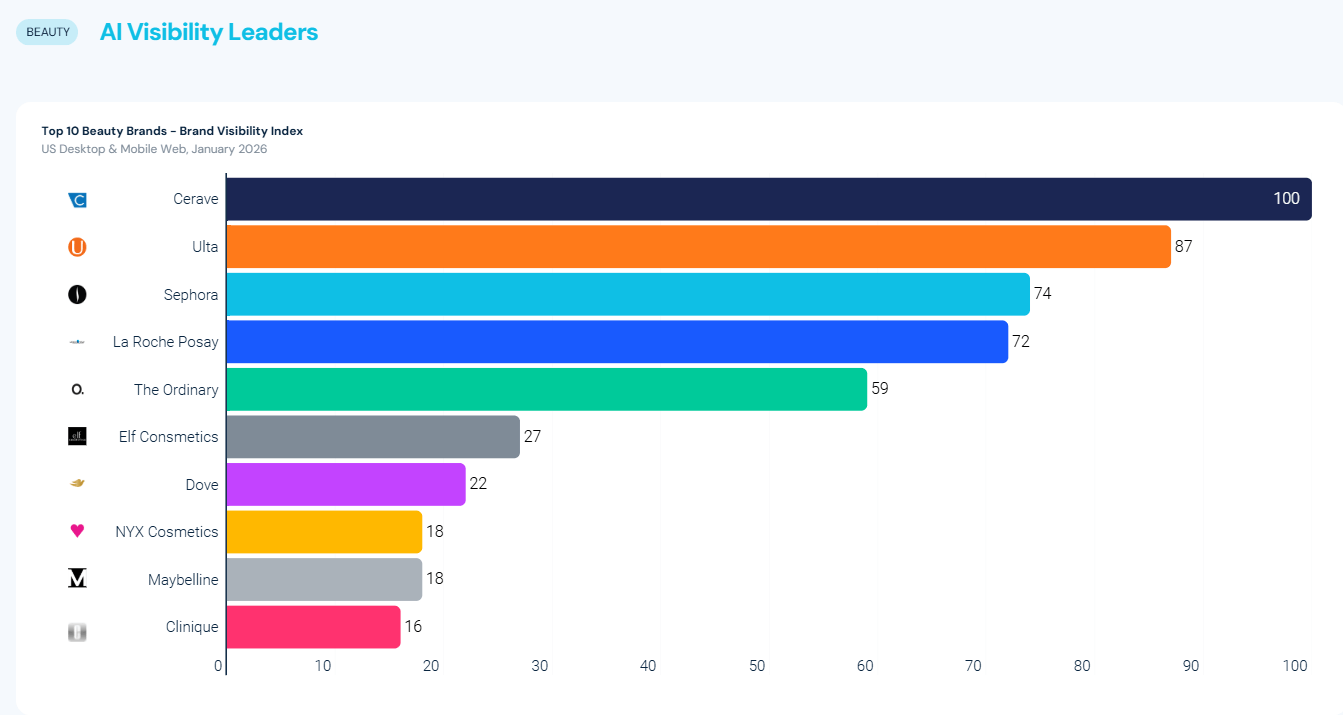

Beauty: education-led skincare dominates over mass cosmetics

CeraVe leads with a 27.17% mention share, not because it has the largest audience (Ulta has ten times the branded search volume), but because dermatologist-recommended, ingredient-focused content is exactly what AI surfaces for skincare questions. The beauty sector is the clearest evidence in the index that AI does not rank brands by popularity. It ranks them by trust signal density.

Mass-market beauty brands with high awareness but shallow ingredient content are structurally disadvantaged in AI, not because AI dislikes them, but because their content does not answer the questions consumers are actually asking.

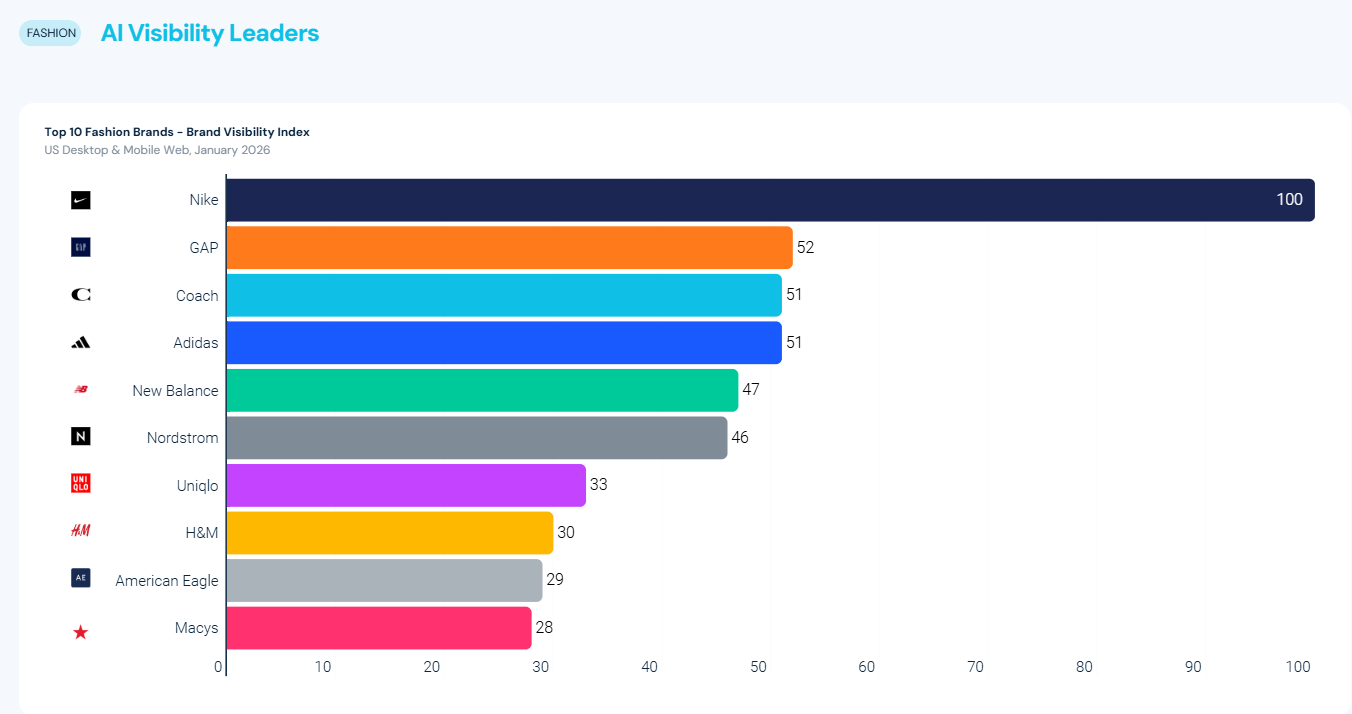

Fashion: athletic and global fast-fashion are winning; heritage retail is not

Nike leads with a 100.0 index score, but its AI visibility momentum is declining (−13.5 from the April 2025 baseline). The actual accelerators are New Balance, Uniqlo, Gap, and H&M. Coach, American Eagle, and Nordstrom are all falling. The Fashion brands gaining AI visibility share are positioned around utility, value, and global relevance, not heritage status.

The pattern suggests AI is absorbing a cultural shift that was already underway in consumer behavior, away from aspirational heritage brands toward accessible, functional, and globally recognizable ones. AI did not create this trend. It is amplifying it.

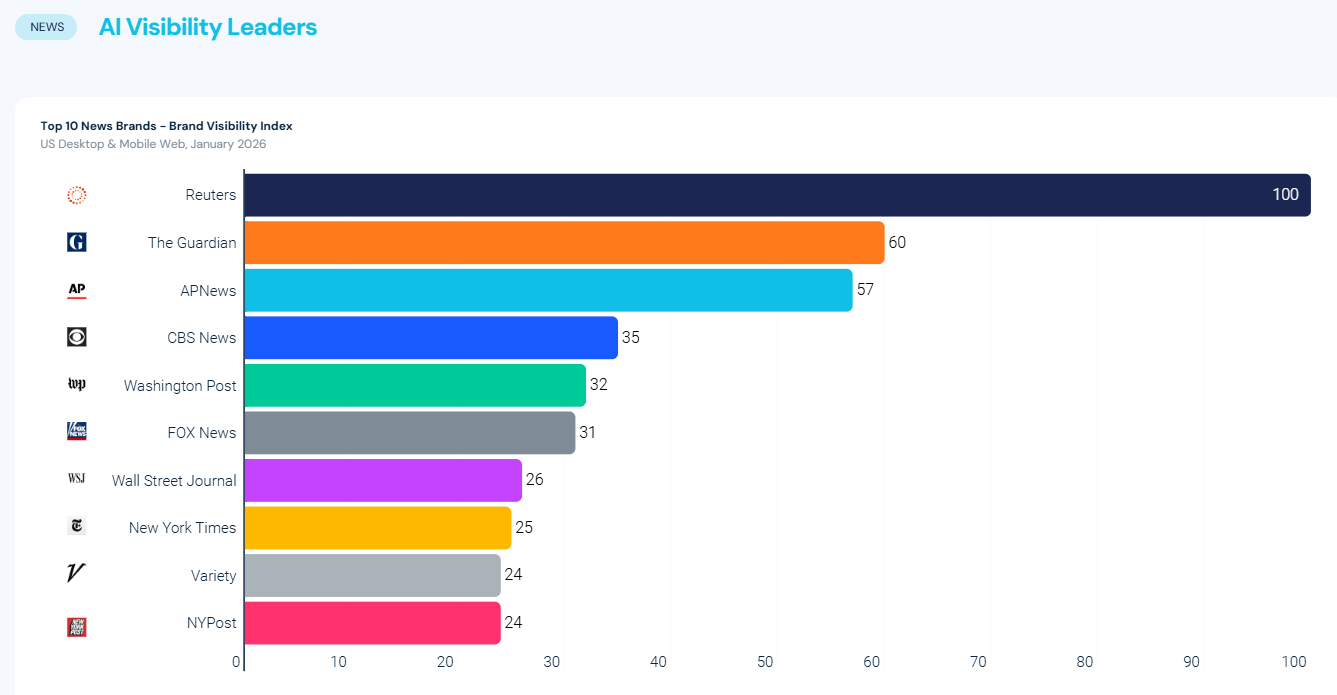

News: the brands blocking AI bots are losing the visibility race

Reuters leads with a 100.0 index score despite just 1.5 million monthly branded searches, far below Fox News (42.1 million), which ranks seventh in AI visibility. Paywalls and AI crawler-blocking remove content from LLM training and retrieval. The New York Times and Wall Street Journal rank eighth and ninth respectively, trailing The Independent and The Guardian. The Guardian’s partnership with OpenAI is a signal of where commercial strategy is heading for the sector.

For news publishers, this is a strategic fork, not a technical one. Blocking AI preserves short-term content control but surrenders long-term influence over how your journalism shapes public knowledge and brand perception.

The overachiever effect: how specialist brands beat household names in AI

The most actionable finding in the 2026 index is not who leads, but who punches above their weight. Across every sector, a consistent category of brands holds AI visibility ranks far higher than their branded search rank would predict.

| Brand | Sector | AI rank | Search rank | Delta |

| WhoWhatWear | Fashion | 27 | 96 | +69 |

| Bankrate | Finance | 13 | 81 | +68 |

| NerdWallet | Finance | 7 | 73 | +66 |

| ScienceDirect | News & Media | 18 | 81 | +63 |

| Travelmath | Travel | 31 | 91 | +60 |

| eCosmetics | Beauty | 26 | 84 | +58 |

| Grailed | Fashion | 31 | 89 | +58 |

| Dermstore | Beauty | 20 | 73 | +53 |

| Adorama | Electronics | 26 | 75 | +49 |

| Swappa | Electronics | 24 | 71 | +47 |

The pattern is consistent across all of them: specialist or niche focus, structured informational content, comparison or reference utility, and lower brand demand than the category leader.

What these brands have in common is not budget or domain authority, it is content design. They built pages that answer specific questions completely, in a format that is easy to extract. That is exactly what LLMs are optimized to retrieve. The overachiever table is, in effect, a blueprint.

The Authority Over Demand (AoD) principle

The overachiever data establishes a principle that runs through the entire index: in AI search, the ability to provide structured, factual, and contextually precise answers outweighs raw brand scale. A mid-size comparison site with well-organized content can appear more frequently in AI responses than a Fortune 500 brand with ten times the search volume. This is not a temporary quirk of early AI behavior. It reflects the fundamental architecture of large language models, which retrieve information based on citation frequency across trusted sources, not based on which brand has the most users.

“The brands leading this index are not accidental winners. They are recognisable brands that have invested consistently in brand equity, category authority, and a durable digital presence. Years of building trust, deep specialism, and recognisable positioning are now compounding in AI search.”, Adelle Kehoe, Director of Product Marketing, Similarweb

Momentum divergence: why your current AI rank may be misleading

A static AI visibility score captures a moment. Momentum data captures a direction. Across all six sectors, Similarweb tracked brand-level AI visibility from April 2025 through January 2026, with the index set to 100 at the start.

| Brand | Sector | Jan 2026 index | Net change | |

| Ulta | Beauty | 319.0 | +219.0 | |

| B&H Photo | Electronics | 296.9 | +196.9 | |

| Washington Post | News | 271.5 | +171.5 | |

| Best Buy | Electronics | 239.7 | +139.7 | |

| Southwest | Travel | 139.9 | +39.9 | |

| NerdWallet | Finance | 134.4 | +34.4 | |

| Nike | Fashion | 86.5 | −13.5 | |

| Airbnb | Travel | 82.8 | −17.2 | |

| Coach | Fashion | 71.5 | −28.5 | |

| AP News | News | 66.1 | −33.9 | |

| WSJ | News | 52.3 | −47.7 |

Ulta’s AI visibility index reached 319 in January 2026, more than triple its April 2025 baseline, through sustained multi-month acceleration, not a single spike. B&H Photo grew nearly 3x over the same period. Both are examples of brands whose content footprint expanded in ways AI retrieval systems reward.

Declining brands tell an equally important story. TripAdvisor dropped to an index of 68.4 despite ranking seventh in the Travel sector overall. The Wall Street Journal fell to 52.3. In News, the brands most exposed to paywall policies and AI crawler restrictions are losing momentum fastest.

The practical implication: a brand holding a strong AI visibility rank today may be in a structurally weakening position if its momentum index is declining. Rank is a lagging indicator. Momentum is the leading one.

The momentum table also reveals something the static rankings hide: some of the fastest-rising brands are not sector leaders, they are mid-table challengers building quietly. B&H Photo ranks seventh in Electronics but has nearly tripled its AI visibility momentum. Washington Post ranks sixth in News but has grown 2.7x. Momentum is where the competitive threat is forming, not at the top of the rankings.

What AI rewards: the content signals driving visibility in 2026

Across all six sectors, the same content characteristics distinguish high-visibility brands from those trailing in AI responses.

Structured, specific, and deep content

A third of ChatGPT citations come from pages three folders deep in a site’s URL structure. A product detail page with a structured “About this item” section outperforms a generic category page. A 2,000-word comparison guide outperforms a 400-word overview.

The implication is counterintuitive for teams trained on SEO: consolidating content into fewer, broader pages works against AI visibility. Depth and specificity beat breadth.

Third-party citation presence

Being authoritative on your own site is necessary but not sufficient. LLMs weigh consensus across sources. Bankrate and NerdWallet in Finance, Travelmath in Travel, WhoWhatWear in Fashion are all cited heavily in third-party editorial content, not just their own domains.

A brand that appears only on its own site looks like a single source. A brand that appears across publishers, review platforms, and community forums looks like a consensus, and consensus is what LLMs are designed to surface.

Accessibility vs. restriction

The News sector data makes a direct case: Reuters, The Independent, and The Guardian, all with open or partially open access, outperform the Times and WSJ in AI visibility despite significantly lower branded search volume. Blocking AI crawlers prevents your content from being included in the retrieval pool.

This is not an argument against paywalls as a business model. It is an argument for being deliberate about which content sits behind them, and ensuring that your most citable, authoritative pages remain accessible.

A 2026 AI visibility content checklist

- Does each key page open with a direct, standalone answer to a specific user question?

- Are product or service attributes explicitly labelled with headers and structured sections?

- Is your brand cited on third-party publisher, review, or UGC platforms, not just your own domain?

- Are your deep pages (3+ folders) as optimized as your top-level pages?

- If you operate a paywall or AI crawler block, have you modeled the AI visibility cost?

- Are you present in the comparison and reference content that dominates your sector?

- Are your FAQ sections structured as standalone Q&A pairs that can be extracted independently?

What to do with this data

The 2026 AI Brand Visibility Index settles several questions that were still open in 2025. AI does not work like search. Brand scale does not guarantee AI visibility. The purchase funnel now starts in AI, not in a search bar. And the brands winning AI responses are often not the brands that won the SEO decade.

The data also identifies what drives AI visibility: structured authority, third-party citation presence, accessible content, and topic-level depth. The same content characteristics that earn Google rankings tend to earn AI citations. The divergence is at the margins, the specialist comparison page, the deep FAQ guide, the editorial presence on trusted third-party sites.

“Everything that works in SEO also works in AEO. What’s new is the head and the tail. To win head keywords in AEO, appearing once at #1 in Google isn’t enough. You win by appearing multiple times across trusted offsite sources so AI models recognize you as a consensus answer. For long-tail keywords, the opportunity is even greater.”, Ethan Smith, CEO, Graphite

Track your brand mention share, measure momentum over time, and build the content that AI systems are structured to trust. Similarweb’s AI Search Intelligence tracks brand mention share and citation frequency across AI platforms, giving teams the data to benchmark performance and monitor changes as retrieval patterns evolve.

FAQs

What is the 2026 Generative AI Brand Visibility Index?

Similarweb’s first report measuring AI brand visibility at the sector level across Finance, Travel, Beauty, Electronics, Fashion, and News. It tracks which brands are named in AI responses across ChatGPT, Gemini, Copilot, and Perplexity, and measures mention share, momentum, and how AI visibility compares to branded search demand, based on US data from January 2026.

What is the current market share of ChatGPT vs Gemini vs Perplexity?

As of September 2025, ChatGPT holds approximately 79% of global Gen AI web traffic. Gemini grew 157% between April and September 2025, reaching 1.1 billion monthly visits. Perplexity reached 170 million monthly visits and Claude 157 million. ChatGPT’s dominance is stable, but Gemini’s growth rate is the most significant competitive shift in the landscape.

How much traffic do AI platforms send to other websites?

Referral volume has plateaued despite rising platform usage. When AI does send traffic, it is high-intent, users referred from ChatGPT convert to transactional sites at 7%, compared to 5% from Google referrals.

Which industries are most visible in AI-generated responses?

Finance has the highest prompt volume (11,073 prompts analyzed), Electronics the most extreme concentration, Apple appears in 54% of all responses. Across every sector, AI visibility does not mirror brand size or search dominance.

Why are some of the biggest brands in their sector losing AI visibility momentum?

Because AI visibility rewards current relevance, not past success. Brands like Nike, Airbnb, and the Wall Street Journal hold strong rankings but declining momentum, their content either does not answer the conversational questions AI retrieves, or their access policies limit what AI can reach. A strong rank can mask a weakening position. Momentum is the earlier warning sign.

If AI referral traffic is flat, why should marketers care about AI visibility at all?

Because influence and a referral click are not the same thing. A consumer asking ChatGPT which brand to trust is making a decision inside the AI response, before any website is visited. The brand named there shapes the shortlist. Waiting for referral volume to justify AI investment means measuring the output of the previous era, not the one you are operating in.

What does the overachiever data tell us about what AI actually values?

That AI does not have brand loyalty, it has content criteria. Specialist sites consistently outrank household names because their content answers specific questions completely, in a format that is easy to extract and verify across multiple sources. The overachievers are not winning on budget or authority. They are winning on content design.

How is AI changing the consumer purchase journey?

AI tools are used by 35% of consumers at the discovery stage versus 13.6% for search, according to Similarweb’s Market Research Panel (US, January 2026). AI holds a 2:1 advantage through every funnel stage until the final purchase step, where the gap closes to near parity. AI starts the journey; search closes the sale.

What content signals does AI reward most?

Structured and specific deep pages, strong third-party citation presence across publishers and UGC platforms, explicit product attribute labelling, and open access for AI crawlers. Brands blocking AI bots or sitting behind paywalls consistently underperform peers with smaller but more accessible content footprints.

Related Posts

Why AI Engines Cite UGC Over Brand Content And How To Leverage It For AEO

AI Mentions vs. AI Citations: What’s the Difference and Why It Matters for GEO

Wondering what Similarweb can do for your business?

Give it a try or talk to our insights team — don’t worry, it’s free!